Early-stage proptech and contech investing: Who gets the VC checks?

Before diving into the topic, I want to make a case for the size and status of the Hong Kong contech (Construction Tech) market:

- From McKinsey: Construction (including real estate, infrastructure, and industrial structures) is the largest industry in the global economy. It accounts for 13 per cent of the world’s GDP.

- From Statista: In 2021, around 326,000 people were employed in Hong Kong’s construction industry. That is 8.5 per cent of the total workforce in Hong Kong.

- From CIC HK: The average age of construction workers in Hong Kong is 47 years old.

Who gets funded and how?

Construction is the biggest industry that provides jobs for many and has been experiencing a rapidly ageing issue in its industrial workforce. With these figures and industry dynamics in mind, contech has become an attractive sector for VC investment. If you camp at HKSTP for three days, you will see a lot of contech startups working on BIM, robotics, DWSS, project management tools, and more.

The real question is — what kind of startups get funded in this space? Having spent some time sourcing deals across different incubators and working on contech deals in the past year, there are three key observations:

Deep industry knowledge and expertise of the founding team

Contech is harder to comprehend than other industries like Consumer, Enterprise Software, and Marketplace for one reason — the nature of the industry. The value chain of construction is complex and involves a lot more parties compared to other verticals.

Compared to an enterprise SaaS salesperson whose typical job involves convincing a client’s BD lead, Product/Project lead, and CFO, contech founders have to be able to comprehend many more pain points that cut across a construction project. Typical that would involve a lot of technical knowledge too. They, therefore, are often faced with a longer sales cycle.

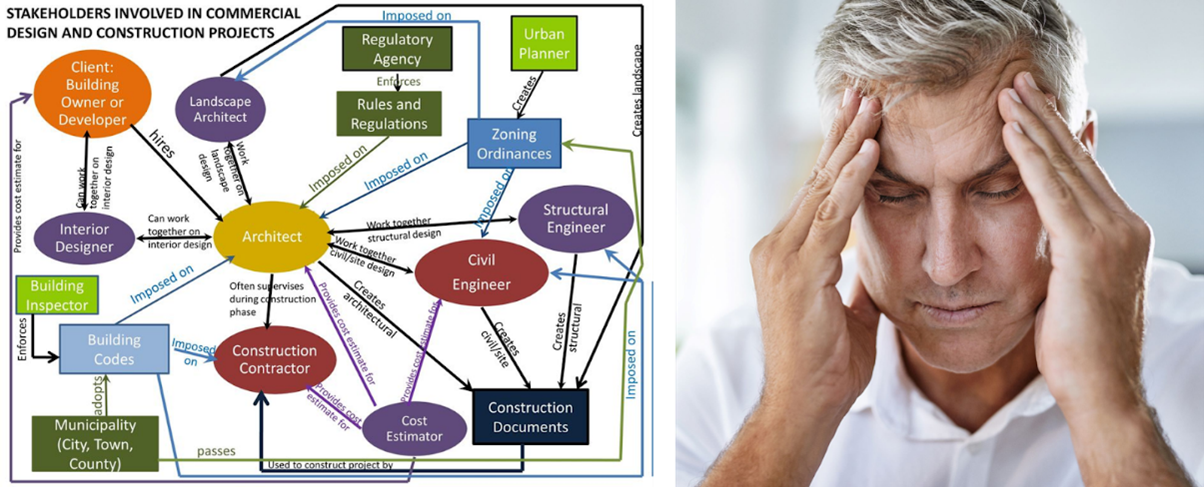

When assessing contech startups, the ability of the founding team members to navigate a complex B2B sales environment is key to their survival and growth. See the photo below about the stakeholder map and my first reaction to the map:

Track record of successful project deliveries before product-led growth

Every single construction project is a prototype itself. Even with a 4D/5D BIM, no one knows how exactly the building will look upon completion on Day 0 when a project starts. This makes creating a product that could be used throughout the asset life cycles of different buildings/infrastructures, or a new service that could be deployed across different stakeholders, harder in contech than in other industries.

Also Read: The tale of the have-yachts and the have-nots in the proptech sector

To prove the value of work and capability of a contech startup, it has to first squeeze in the radar of potential clients and get noticed. That is why I believe contech startups will inevitably go through a longer period of being a “consulting-ish” company compared to B2B SaaS startups operating in other verticals.

A “consulting-ish” company is the stage where a startup is trying to become a product company but has to take project-based income to buy time to reach product-market fit. Contech startups who haven’t gone through this stage will either be category-defining stars or completely irrelevant to the game.

Opportunities lie in the earlier parts of the value chain

Let’s break down the value chain of a construction project into three parts:

- Pre-construction

- During-construction

- Post-construction.

In general, I think the density of capital is much higher in the first two bits compared to post-construction.

The math in my mind is simple: the first two are big lump-sum from developers/main contractors/owners, while the third one is money from individual tenants paying management fees. An over-generalised thought of mine is that the likelihood of a startup grabbing a small bite and becoming a scale-up by operating in first and/or second is higher than operating only in third.

Founders operating in contech will understand the stark difference in customers’ ability to pay across the value chain. The photo below shows the relative sizes of funding in the US contech market from 2000 to 2021. Founders – pick your battles!

The relative sizes of Contech categories

The above is, of course, an oversimplified view of the contech startup space. Many successful startups just break existing assumptions and prove investors wrong.

If you have a contech startup idea and are operating in HK/GBA, I would love to learn more.

–

Editor’s note: e27 aims to foster thought leadership by publishing views from the community. Share your opinion by submitting an article, video, podcast, or infographic

Join our e27 Telegram group, FB community, or like the e27 Facebook page

Image credit: 123rf-nexusplexus

The post Early-stage proptech and contech investing: Who gets the VC checks? appeared first on e27.